Why Cash Sales Close Faster: A Guide for Urgent Sellers

TL;DR:

- Cash sales close faster because they eliminate mortgage underwriting, appraisals, and approval delays. A cash transaction can wrap up in 7 to 14 days, compared to 30 to 45 days for financed deals. This speed provides financial certainty, especially for homeowners facing urgent circumstances.

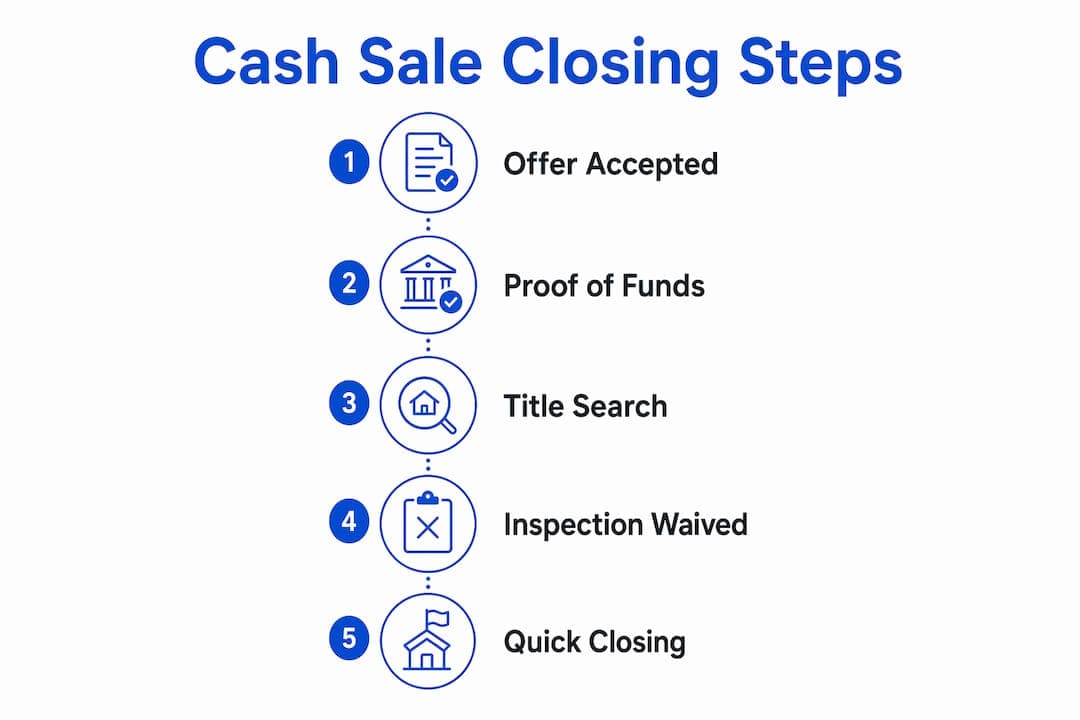

Cash sales close faster than financed transactions because they eliminate mortgage underwriting, lender appraisals, and approval delays that routinely add weeks to a deal. A financed closing typically takes 30–45 days; a cash transaction with a clean title can wrap up in 7–14 days. For homeowners facing foreclosure, estate settlement, or a job relocation, that difference is not just convenient. It is often the difference between financial stability and serious loss. Understanding why cash sales close faster gives you real leverage when time is your most limited resource.

Why cash sales close faster: no lender, no waiting

The single biggest reason cash transactions move quickly is the complete removal of lender involvement. When a buyer uses a mortgage, the deal depends on the lender’s schedule, not yours. Underwriting alone can take two to three weeks, and that clock does not start until the buyer submits a full application.

Cash purchases eliminate every step tied to a lender. There is no pre-approval to wait on, no underwriting file to build, and no lender-ordered appraisal to schedule. Cash purchases close in 7–14 days with no lender involvement, compared to 30–45 days for most mortgage closings. That gap represents weeks of mortgage interest, property taxes, and maintenance costs you no longer have to carry.

Verified funds also reduce the risk of a deal falling apart at the last minute. Cash buyers have funds verified upfront, which cuts the deal-collapse risk that financed buyers carry when their loan approval falls through. For a seller in a tight spot, that certainty is worth more than a slightly higher offer price that might never reach the closing table.

Key steps removed when a buyer pays cash:

- Mortgage pre-approval and application processing

- Lender-ordered home appraisal

- Underwriting review and conditional approval

- Lender-required repairs before funding

- Final loan commitment and funding authorization

Each item on that list represents days or weeks. Remove them all, and the path from accepted offer to closed sale becomes very short.

How fewer contingencies speed up the closing process

Contingencies are conditions that must be met before a sale can close. In financed deals, buyers routinely include financing contingencies, appraisal contingencies, and inspection contingencies. Each one creates a window where the deal can stall or collapse.

Cash buyers tend to waive appraisal and financing contingencies, which removes two of the most common delay sources in a traditional sale. A financing contingency alone can extend a deal by two weeks if the buyer’s lender pushes back on approval. An appraisal contingency adds another round of negotiation if the appraised value comes in below the purchase price.

Cash buyers purchase homes as-is and factor the property’s condition directly into their offer. That approach skips the repair negotiation cycle entirely. In a financed deal, a buyer’s inspector might flag ten items, the buyer requests repairs, you negotiate, and then the lender may require some of those repairs before funding. That back-and-forth can add two to four weeks to a closing timeline. Selling as-is saves significant time when you need to move quickly.

Pro Tip: Before accepting any cash offer, confirm the buyer has a proof-of-funds letter from a bank or financial institution. Verbal assurances do not protect you if the deal falls through at closing.

The practical result of fewer contingencies is a shorter, cleaner contract. Fewer conditions mean fewer opportunities for delays, renegotiations, or deal collapses. For homeowners who need a firm closing date, a low-contingency cash offer delivers far more certainty than a financed offer loaded with conditions.

What can still slow down a cash sale?

Cash removes lender delays, but it does not eliminate every possible obstacle. Title issues are the leading cause of delays in cash transactions, and they can push a closing back by weeks regardless of how prepared the buyer is.

Title problems like liens, judgments, and boundary disputes are the biggest remaining variable in a cash sale. A property with unpaid contractor liens, back taxes, or unclear ownership history cannot close until those issues are resolved. A clean title enables closings in as little as 3–7 days, while title defects can push that timeline past 21 days even when the buyer has cash in hand. Understanding the role of a title company in this process helps you prepare before you list.

Common title problems that delay cash closings:

- Unpaid property tax liens from prior years

- Contractor or mechanic’s liens from past work

- Unresolved judgments against the property owner

- Errors in public records or deed descriptions

- Ownership disputes from estate or divorce proceedings

Pro Tip: Order a preliminary title search before you accept any offer. Most title companies complete this within 48–72 hours, and it gives you time to resolve problems before they delay your closing.

Buyer preparedness also matters. An experienced cash buyer with verified funds and a reliable title company moves faster than a first-time cash buyer who is unfamiliar with the process. Verified funds and experienced cash buyers reduce friction and unexpected contingencies, which is why working with established cash buyers consistently produces faster results than accepting a cash offer from an unknown party.

Financial benefits of a faster closing for urgent sellers

Speed has a direct dollar value for homeowners carrying a property they need to exit. Every month a home sits on the market costs money. Mortgage payments, property taxes, homeowner’s insurance, and basic maintenance add up fast.

Selling quickly to a cash buyer cuts carrying costs immediately, stopping the financial bleed from ongoing monthly expenses. For a homeowner already stretched thin, avoiding two or three extra months of payments can be more valuable than holding out for a higher offer price. A free home valuation can help you understand exactly what your property is worth before you decide which offer to accept.

The financial advantages of a fast cash closing include:

- No additional mortgage interest payments during a prolonged listing period

- No agent commissions, which typically run 5%–6% of the sale price

- No repair costs required to satisfy a lender or financed buyer

- No staging, photography, or open house expenses

- Elimination of double mortgage payments if you have already purchased your next home

For homeowners in urgent situations, the control over exit timing that a cash sale provides often outweighs any price concession. If you are facing foreclosure, the ability to close in seven days and protect your credit history is worth far more than waiting 60 days for a financed buyer who might offer slightly more. Homeowners comparing a cash sale versus foreclosure outcome consistently find that speed preserves more long-term financial health.

Cash sales also reduce the emotional cost of selling. Cutting months of uncertainty from an estate or relocation sale removes the stress of shared decisions, repeated showings, and drawn-out negotiations. For sellers managing grief, job transitions, or financial pressure, that reduction in stress has real practical value.

Key Takeaways

Cash sales close faster than financed transactions because they eliminate lender underwriting, appraisals, and contingencies, cutting closing timelines from 30–45 days down to 7–14 days.

| Point | Details |

|---|---|

| No lender involvement | Cash sales skip underwriting and appraisals, closing in 7–14 days versus 30–45 for financed deals. |

| Fewer contingencies | Cash buyers typically waive financing and appraisal conditions, removing the most common delay sources. |

| Title clarity is critical | A clean title enables closings in 3–7 days; unresolved liens or disputes can push timelines past 21 days. |

| Financial savings add up | Faster closings eliminate carrying costs, agent commissions, and repair expenses that erode your net proceeds. |

| Verified funds matter | Confirmed buyer liquidity reduces deal-collapse risk and keeps the closing timeline on track. |

What I’ve learned from watching urgent sellers choose cash

Speed is the right priority for more sellers than conventional real estate advice admits. The standard guidance tells homeowners to list on the open market, wait for the highest offer, and negotiate from strength. That advice works well when you have time. When you do not, it can cost you far more than the price difference between a cash offer and a financed one.

The sellers I have seen benefit most from cash transactions share one trait: they know their real priority before they start. If your goal is maximum price and you have 60 days to spare, a traditional listing makes sense. If your goal is a firm closing date and financial certainty, a cash offer wins almost every time.

The caveat I always raise is buyer verification. Not every “cash buyer” is equally prepared. Some investors make verbal cash offers without confirmed funds, which creates the same deal-collapse risk as a financed buyer. Insisting on a proof-of-funds letter before signing anything is non-negotiable.

Title readiness is the other factor sellers consistently underestimate. Ordering a preliminary title search early gives you time to clear liens or correct record errors before they become closing emergencies. Sellers who do this arrive at the closing table with confidence instead of surprises.

The bottom line is straightforward. Cash sales offer speed, certainty, and financial control that financed transactions cannot match. For homeowners in urgent situations, those three things are worth more than a marginally higher offer price that takes twice as long to close.

— Bryan

Housegoodbye makes fast cash sales real for Michigan homeowners

Housegoodbye connects Michigan homeowners with multiple competing cash investors, so you receive real offers quickly without the delays of a traditional listing. You sell your property as-is, with no repairs, no staging, and no agent commissions eating into your proceeds.

The process is direct: submit your property details, receive competing cash offers in Michigan, and choose the offer that fits your timeline. Housegoodbye’s verified buyers can close in as little as seven days, which matters most when foreclosure, relocation, or estate deadlines are driving your decision. If you want to sell your house as-is without the usual hassle, Housegoodbye gives you a clear, fast path to closing.

FAQ

Why do cash sales close faster than financed sales?

Cash sales eliminate mortgage underwriting, lender appraisals, and financing contingencies. Those steps alone account for most of the 30–45 day timeline in a financed closing.

How fast can a cash sale actually close?

A cash sale with a clean title can close in as little as 3–7 days. Title defects like liens or ownership disputes can extend that timeline past 21 days even with a ready cash buyer.

Do cash buyers always buy homes as-is?

Most cash buyers purchase properties as-is and factor condition into their offer price. This removes repair negotiations and lender-required fix requirements that commonly delay financed deals.

What is the biggest risk in a cash sale?

Unverified buyer funds and title defects are the two main risks. Always request a proof-of-funds letter and order a preliminary title search before accepting any cash offer.

Can a cash sale still fall through?

Yes, though it is far less common than with financed deals. The most frequent causes are unresolved title issues, buyer fund problems, or unexpected inspection findings that the buyer uses to renegotiate.