Navigating tax rules when selling your home during or after a divorce can be tricky. This guide makes the home sale exclusion easy to understand, helping you save money.

Key Takeaways

Here are the most important things to remember about home sale taxes and divorce. It is smart to know the rules when selling your home during a divorce. There are tax benefits to help you save money. You can exclude money gained from the sale of your home from taxes.- Exclusion Caps: Single people can exclude up to $250,000 from their taxes. Married couples filing together can exclude up to $500,000.

- Divorce Impact: Divorce changes your tax filing status. This can lower the amount you can exclude.

- Two-Year Rule: You must have owned your home and lived in it as your main home for at least two of the last five years. This rule is key for the tax break.

- Plan Ahead: Talk to a tax advisor or lawyer early. This can help you save more cash and follow the rules correctly. Understanding current IRS home sale rules is vital.

Understanding the Home Sale Exclusion Basics

The home sale exclusion saves you taxes on profits when you sell your main house. When you sell your main home, you might make money. This money is called a "capital gain." The U.S. government (IRS) has a special tax rule. It lets you keep some of this profit without paying federal income tax (the tax on your wages or earnings). This rule is called the home sale exclusion. This tax break can be very helpful for many people. It is key during big life changes, like getting a divorce. It helps you keep more of your money.How Much Can You Exclude?

The amount of profit you can exclude depends on your tax filing status.- Single Filers: You can exclude up to $250,000 of profit.

- Married Couples Filing Jointly: You can exclude up to $500,000 of profit.

Who Qualifies for the Exclusion?

To use this exclusion, you must meet two main rules from the IRS:- Ownership Test: You must have owned the home for at least two years. This period must be within the five years before you sell it. For example, if you sell in 2024, you must have owned it for at least two years between 2019 and 2024.

- Use Test: The home must have been your main home for at least two years. This period also must be within the five years before you sell it. Your "main home" is where you live most of the time. This means if you have multiple homes, this is the one you use most often.

How Divorce Affects Your Home Sale Exclusion: Key Rules

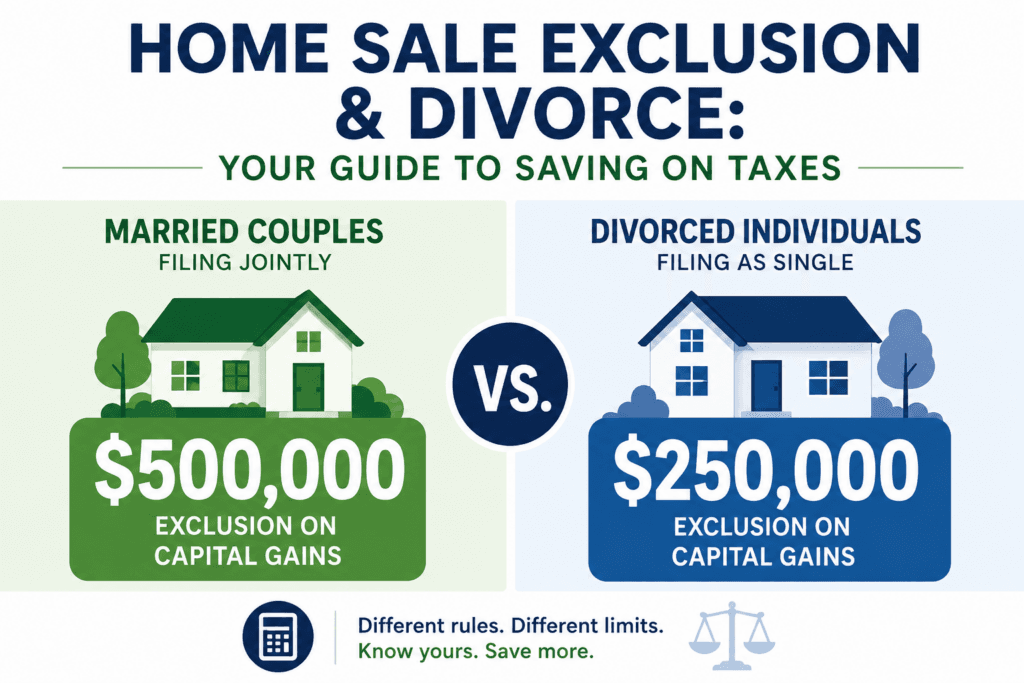

When you sell your home, the rules for saving on taxes change after a divorce. After a divorce, your tax filing status changes. This directly affects how much profit (gain) you can exclude from taxes when you sell your home. For married couples filing jointly, you can exclude up to $500,000 of profit. Once divorced, each person is generally limited to a $250,000 exclusion.

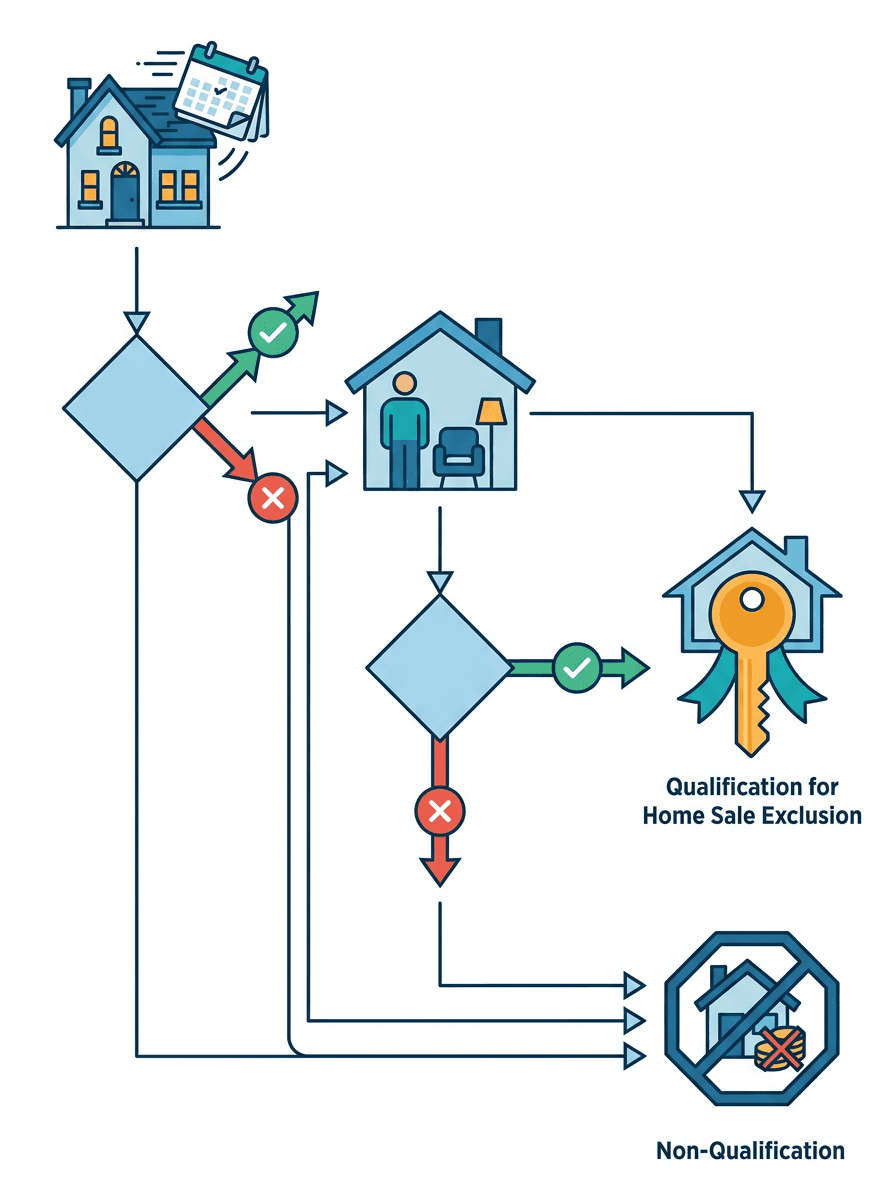

Flowchart explaining the two main tests (ownership and use) required to qualify for the home sale tax exclusion.

The Ownership and Use Tests After Divorce

The IRS has specific rules for who can claim this tax saving. These are called the "ownership test" and the "use test." You must meet both tests to qualify for the exclusion.Ownership Test

You must have owned the home for at least two years. This means you held the title or deed. For divorce, this still applies. Even if only one person's name was on the deed, if the divorce agreement says both owned it, the IRS might accept that.Use Test

You must have lived in the home as your main residence for at least two years. This is out of the last five years before you sell it. This rule can get tricky with divorce. What if one person moves out? The IRS has a special rule for divorced couples. If you moved out but your ex-spouse continues to live in the home and you still own your share, you might still meet the use test. The divorce or separation agreement needs to state this. This lets the person who moved out still count their time living there through their ex-spouse. For example, if you move out in 2020 but your ex-spouse lives in the home until you sell it in 2023, you still meet the use test if your divorce papers confirm your ownership. This lets you claim your $250,000 exclusion.Selling Before or After Divorce

The timing of your home sale around your divorce matters a lot for taxes.- Selling Before Divorce is Final: If you sell your home before your divorce is officially final, the IRS still sees you as married. This means you can still claim the larger $500,000 exclusion. This can be a smart move for some families. Many people choose to sell their home quickly before the divorce is final to take advantage of this larger exclusion. HouseGoodbye.com can help you sell your house fast for cash, which might be helpful in this situation.

- Selling After Divorce is Final: Once your divorce is final, each person is treated as single for tax purposes. Each ex-spouse can exclude up to $250,000 of profit from their share of the sale. This applies even if you owned the home together for many years before the divorce.

- Before Divorce: John and Mary sell their home together. They made a profit of $400,000. Since they are still married, they can exclude all $400,000. They pay no tax on this gain.

- After Divorce: John and Mary divorce. They then sell their home and split the $400,000 profit evenly, so each gets $200,000. Each person can exclude their $200,000 profit. They still pay no tax.

- After Divorce, Higher Gain: What if they made a profit of $600,000? Each gets $300,000. Each can exclude $250,000. But the remaining $50,000 for each person (total $100,000) will be taxable as a capital gain. For more details, you can visit the IRS website on selling your home.

How to Avoid Capital Gains if Bought Out of Home Due to Divorce?

If your spouse buys out your share of the home due to divorce, you typically don't pay capital gains tax.

Diagram illustrating a tax-free home transfer during divorce, with the receiving spouse incurring capital gains upon later sale.

When you divorce, transferring property between you and your spouse usually has no tax. This is thanks to IRS Section 1041. This rule means you don't pay tax when you give or receive property from your spouse or former spouse if it's done because of your divorce.

Let's say your spouse keeps the family home. You sign over your ownership to them. You will not owe capital gains tax at that time. Think of it as a gift. The IRS does not tax gifts between spouses during a divorce.

Understanding "Tax Basis"

The spouse who receives the home also takes on its "tax basis." The tax basis is the original cost of the home plus the cost of certain improvements. Imagine you bought a house for $200,000. You spent $50,000 on approved upgrades. Your tax basis is now $250,000. If your spouse gets the house, their tax basis is also $250,000. When they later sell the house to someone else, the capital gains are figured from that $250,000 basis. This means they are responsible for the tax on any profit made from that point forward.Your Divorce Agreement Matters

A strong divorce agreement is very important. This legal paper should clearly state who gets the home and how the transfer happens. It protects both you and your ex-spouse. It guides the transfer and helps prevent future tax surprises. You can learn more about how agreements impact selling a property by reading about selling a house without a realtor. Make sure your agreement covers these points:- Who owns the home: Clearly name the spouse who will keep the house.

- Transfer date: The exact date the ownership changes hands.

- Fair market value: The agreed-upon price of the home at the time of transfer.

Get Expert Help

Divorce and taxes can be tricky. It's smart to talk to a tax advisor and a lawyer. They can help you structure the home buyout to save money on taxes for both people. Having experts on your side can make the process smoother. They will explain specific rules for your situation. The IRS Publication 523 offers more details on selling your home and exclusions. Finding good advice upfront can help prevent costly mistakes later. This is often true when you are navigating a house sale during life changes.Why Moving Out Isn't Always the Biggest Mistake in a Divorce

It's not always a mistake to move out during your divorce; proper planning can protect your financial interests. Many people believe that moving out of the marital home during a divorce automatically gives up rights. This is a common myth. While it feels like a big step, leaving the house does not always mean you lose out financially. This is especially true when it comes to the home sale exclusion.The Home Sale Exclusion and "Deemed" Use

The "home sale exclusion" lets you avoid paying taxes on some of the money you make when you sell your house. As a single person, you can exclude up to $250,000 of profit. A married couple can exclude up to $500,000. To get this benefit, you must have owned and lived in the home for at least two of the last five years. These are called the "ownership" and "use" tests. Moving out usually means you no longer "use" the home. However, the IRS has a special rule for divorced couples. If your divorce or separation agreement says your former spouse can live in the home, you can still meet the "use test." This is called "deemed use." It means the time your ex-spouse lives there counts as your time, too. This protects your right to the tax exclusion when the house sells.When Moving Out Makes Sense

There are many good reasons to move out, even during a divorce.- Emotional Well-being: Living in a stressed home environment can be very hard. Moving out can create a more peaceful space for you and your children.

- Safety: If there is conflict or abuse, moving out is often necessary for safety. Your well-being comes first.

- New Beginnings: Sometimes, starting fresh in a new place helps you move forward. It can reduce daily arguments.

Protect Your Rights with Agreements

The key to protecting your financial stake is a clear divorce agreement. This legal document should spell out many things. It covers how the house will be handled, including who stays and for how long. It also mentions how sale profits, including the tax exclusion, will be split. Make sure your attorney includes details about the home sale. This will protect your ability to claim the home sale exclusion, even if you move out. Without a formal agreement, it can be much harder to claim your share of the exclusion. For more general information on selling your home during a divorce, explore IRS Publication 523. Need to sell your house fast during or after a divorce? HouseGoodbye.com helps homeowners sell their properties quickly and easily. Learn more about how we can help you sell your house fast for cash.The Capital Gains Exclusion After Divorce: What You Need to Know

After divorce, each person gets their own $250,000 tax break when selling the house. After a divorce, the rules for your home sale tax break change. As an unmarried person, you can exclude up to $250,000 of profit from your income tax. For couples, this tax-free amount was up to $500,000. Once divorced, each ex-spouse typically gets a $250,000 exclusion.

Capital gains tax exclusions for a married couple versus two divorced individuals ($500,000 vs. two $250,000 exclusions).

This can be a problem if your home increased a lot in value. For example, imagine you and your ex-spouse bought a home for $300,000. You sell it for $900,000, making a $600,000 profit. If you were still married, you would pay no tax on that $600,000 profit. After divorce, each of you can only exclude $250,000. This leaves $100,000 of profit that will be taxed. Even if one spouse keeps the home for a bit and then sells it, they still only get the $250,000 exclusion.

There are ways to plan around this. One option is to sell your home before your divorce is final. If you are still legally married when you sell, you can claim the full $500,000 exclusion. This requires both people to agree and work together. This can save a lot of money in taxes.

Here's how selling before divorce can help:

- Higher Exclusion: You can exclude up to $500,000 of profit.

- Less Tax: You pay less capital gains tax, or none at all.

- More Cash: You keep more of the sale money.

Co-Owning Your Home After Divorce: Tax Implications

It's common for ex-spouses to own their home together after a divorce, but this can affect your tax savings later. Sometimes, ex-spouses continue to own a home together. This might happen if homes aren't selling well, or if children need to finish school. You both stay on the title, even if only one person lives there. When you sell the home later, the home sale exclusion still applies. Each person can exclude up to $250,000 of profit. This is true even if one person moved out. The IRS allows an exception for former spouses. If your divorce papers say one person can live in the home, the other person counts as "using" the home. This "deemed use" helps both ex-spouses qualify for the tax break. For example, if you sell your home and make $400,000 profit, and you both meet the rules, neither of you would pay tax on the profit. This is because each of you can exclude up to $250,000. Your combined exclusion is $500,000, which covers the $400,000 gain. To learn more about this rule, check out IRS Publication 523, Selling Your Home. It is very important to have a clear agreement about co-owning the home. This agreement should be part of your divorce papers. It should cover:- Who pays what? Decide who handles mortgage payments, property taxes, and repairs.

- When to sell? Set a date or event for when the house must be sold.

- How to split money? Explain how profits and costs will be shared.

Reporting the Sale of Your Home After Divorce

It's important to report your home sale correctly to the IRS after a divorce. After your divorce, selling your home has tax steps. You need to tell the IRS about this sale. This helps you claim your proper tax exclusions. Key Forms to Use You will likely need these two IRS forms:- Form 8949: This form lists sales of capital assets. Your home is a capital asset. You will put details about your home sale here.

- Schedule D: This form summarizes your capital gains and losses. Information from Form 8949 flows to this schedule.

- Original Purchase Price: The amount you and your ex-spouse first paid for the house.

- Cost of Improvements: Money spent on major repairs or upgrades. This includes things like a new roof or a kitchen remodel. These costs add to your "basis" (your total investment).

- Selling Expenses: Costs related to the sale. Examples are real estate agent fees and legal fees.

- Sale Price: The final amount your home sold for.

- Form 1099-S: You might get this form from your closing agent. It shows the gross proceeds from your sale.

- Gather Documents: Collect your original purchase papers and improvement receipts.

- Find Sale Details: Get your closing statement. It shows the sale price and selling costs.

- Check for Form 1099-S: See if you received this form.

- Calculate Your Basis: Add your purchase price and improvement costs.

- Figure Your Gain: Subtract your basis and selling expenses from the sale price.

- Complete Form 8949: Enter your home sale details.

- Fill out Schedule D: Transfer totals from Form 8949.

Special Considerations: Over 55 Home Sale Exemption & Other Rules

You need to know how special rules affect your home sale tax benefit, especially if you are over 55. Many people remember an "over 55 home sale exemption." This rule is actually outdated. Before 1997, sellers over age 55 could exclude a one-time gain of $125,000 from their home sale. However, current tax law replaced this with the Section 121 exclusion. This new rule lets most homeowners exclude up to $250,000 in gain ($500,000 for married couples). It applies regardless of age, as long as you meet other rules. The IRS has specific rules for this home sale exclusion. To qualify for the full exclusion, you must:- Own the home: You must have owned your home for at least two years.

- Live in the home: You must have used it as your main home for at least two years. This "use" time must be within the five years before you sell it.

- A job change in a new location.

- Health problems that require you to move.

- Unforeseen events, like a natural disaster.

Home Sale Exclusion Divorce: Actionable Steps & Timelines

To save on taxes when selling your home during a divorce, make decisions early and get expert advice. Selling your home during a divorce brings unique tax rules. The timing of your home sale matters a lot. Making smart choices can save you thousands of dollars. It’s vital to get advice before your divorce is final. Gathering home financial records is a key first step. These papers show your home's original cost and money spent on upgrades. You will need:- Purchase price info: The amount you paid for the home.

- Improvement receipts: Records for any major fixes or upgrades. This includes things like a new roof or kitchen remodel.

- Selling cost estimates: Think about agent fees or closing costs.

Your Home Sale Timeline During Divorce

The best time to sell your home for tax savings is usually before your divorce is final. If you sell as a married couple, you can exclude up to $500,000 of profit. If you sell after the divorce, each person can only exclude up to $250,000. This could mean a big difference in taxes owed. Consider this example. A couple sells their home before divorce and makes $400,000 profit. They pay no taxes on this. If they sold after divorce, splitting the profit, each would get $200,000. Each would still pay no taxes. But if they made $600,000 profit, selling before divorce means no taxes. Selling after divorce, each gets $300,000. Each would then pay taxes on $50,000.Crucial Steps for Selling Your Home During Divorce

A smooth sale during divorce needs planning. Work with experts. They can guide you through the process. A divorce attorney helps with legal forms. A tax professional understands tax rules. Here is a checklist of steps to take:- Get legal advice early. Talk to a divorce lawyer as soon as possible. They help you understand your rights and options.

- Consult a tax expert. A tax advisor can explain how the home sale exclusion works for you. Ask about your specific money situation.

- Decide on timing. Discuss with your attorney and ex-spouse if selling before or after divorce is best.

- Collect all home documents. Gather purchase agreements, receipts, and appraisal reports. This helps prove your costs.

- Value your home. Get a professional appraisal to know your home's current market value.

- Consider selling your house for cash. Companies like HouseGoodbye.com can buy your home fast, without repairs or agent fees. This can make the process simpler.